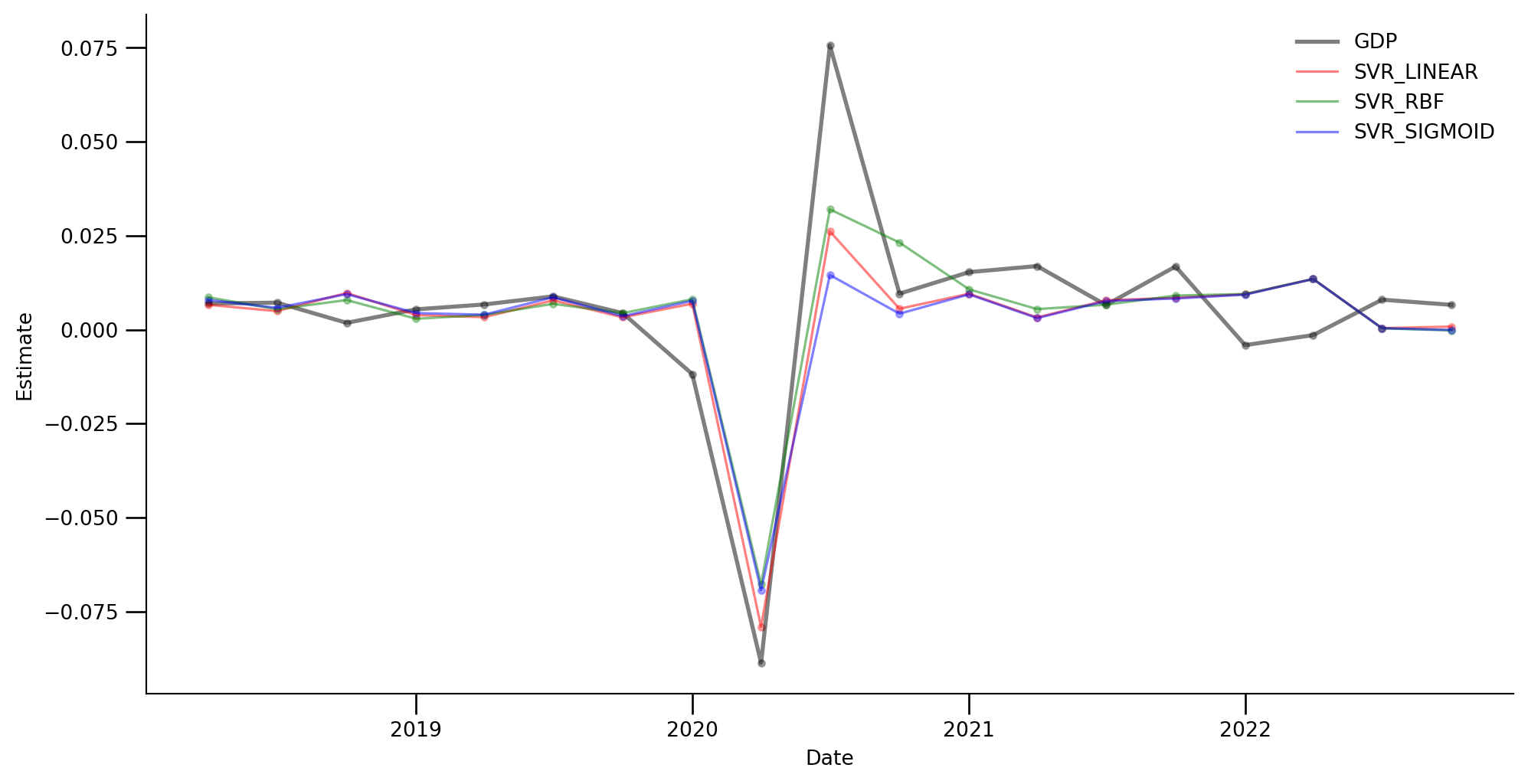

Code

from matplotlib.ticker import MultipleLocator, AutoMinorLocator

from matplotlib.dates import YearLocator

import matplotlib.pyplot as plt

import pandas as pd

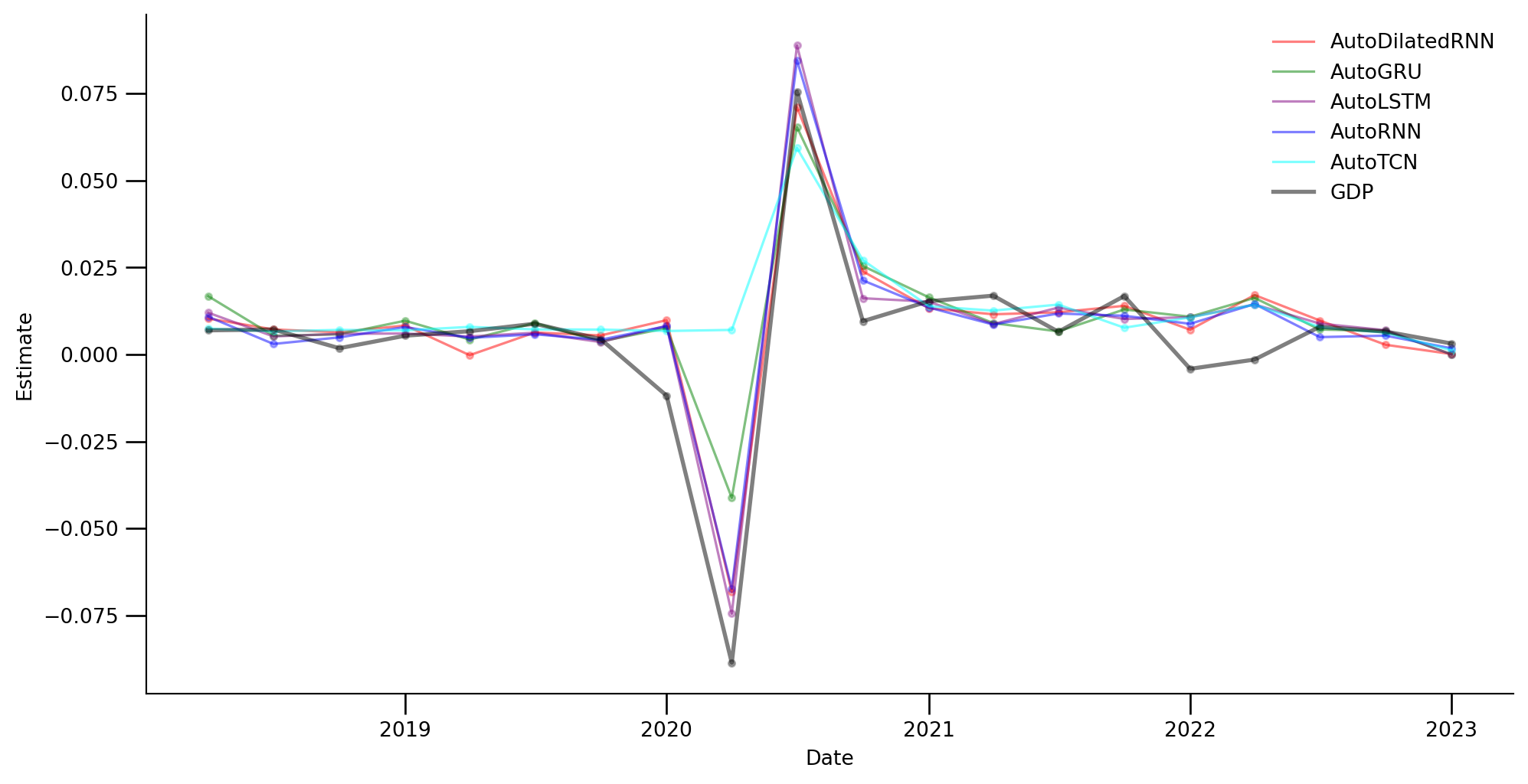

data = pd.read_csv('../presentation/01_data/tidy_svr.csv')

data['ds'] = pd.to_datetime(data['ds'])

models_to_plot = ['SVR_LINEAR', 'SVR_RBF',

'SVR_SIGMOID', 'GDP']

filtered_data = data[data['Model'].isin(models_to_plot)]

grouped = filtered_data.groupby('Model')

selected_data = pd.concat([group.iloc[::3] for _, group in grouped])

model_color_dict = {

'SVR_LINEAR': 'red',

'SVR_RBF': 'green',

'SVR_SIGMOID': 'blue',

'GDP': 'black'

}

fig, ax = plt.subplots(figsize=(12, 6))

ax.xaxis.set_major_locator(YearLocator())

ax.spines['top'].set_visible(False)

ax.spines['right'].set_visible(False)

ax.tick_params(which="major", width=1.0)

ax.tick_params(which="major", length=10)

ax.tick_params(which="minor", width=1.0, labelsize=10)

ax.tick_params(which="minor", length=5, labelsize=10, labelcolor="0.25")

ax.set_ylabel("Estimate", weight="medium")

ax.set_xlabel("Date", weight="medium")

default_linewidth = 1.2

gdp_linewidth = 2

for model in selected_data['Model'].unique():

subset = selected_data[selected_data['Model'] == model]

ax.scatter(subset['ds'], subset['Estimate'], s=10, color=model_color_dict[model],

edgecolor=model_color_dict[model], linewidth=1, zorder=-20, alpha=0.3)

linewidth = gdp_linewidth if model == 'GDP' else default_linewidth

ax.plot(subset['ds'], subset['Estimate'],

c=model_color_dict[model], linewidth=linewidth, alpha=0.5, label=model)

ax.legend(frameon=False)

plt.show()