TFRE package¶

TFRE.TFRE module¶

A Tuning-free Robust and Efficient (TFRE) Approach to High-dimensional Regression

- class TFRE.TFRE.TFRE[source]¶

A class used to perform TFRE regrssions

- Returns:

model (TFRE.model class) – The class used to record the regression details.

TFRE_Lasso (TFRE.Lasso class) – The class used to record the results of the TFRE regrssion with Lasso penalty.

TFRE_scad (TFRE.SCAD class) – The class used to record the results of the TFRE regrssion with SCAD penalty.

Noneifsecond_stageis notscad.TFRE_mcp (TFRE.MCP class) – The class used to record the results of the TFRE regrssion with MCP penalty.

Noneifsecond_stageis notmcp.

- class Lasso(beta_TFRE_Lasso, tfre_lambda)[source]¶

a class used to record the results of the TFRE regrssion with Lasso penalty.

- Returns:

beta_TFRE_Lasso (np.ndarray([p+1,])) – The estimated coefficient vector of the TFRE Lasso regression. The first element is the estimated intercept.

tfre_lambda (np.ndarray([1,])) – The estimated tuning parameter of the TFRE Lasso regression.

- class MCP(Beta_TFRE_mcp, df_TFRE_mcp, eta_list, hbic, min_ind)[source]¶

a class used to record the results of the TFRE regrssion with MCP penalty.

Noneifsecond_stageis notmcp.- Returns:

Beta_TFRE_mcp (np.ndarray([k,p+1])) – The estimated coefficient matrix of the TFRE MCP regression. The diminsion is k x (p+1) with the first column to be the intercepts, where k is the length of

eta_listvector.df_TFRE_mcp (np.ndarray([k,])) – The number of nonzero coefficients (intercept excluded) for each value in

eta_list.eta_list (np.ndarray([k,])) – The tuning parameter vector used in the TFRE MCP regressions.

hbic (np.ndarray([k,])) – A numerical vector of HBIC values for the TFRE MCP model corresponding to each value in

eta_list.eta_min (float) – The eta value which yields the smallest HBIC value in the TFRE MCP regression.

beta_TFRE_mcp_min (np.ndarray([p+1,])) – The estimated coefficient vector which employs

eta_minas the eta value in the TFRE MCP regression.

- class SCAD(Beta_TFRE_scad, df_TFRE_scad, eta_list, hbic, min_ind)[source]¶

a class used to record the results of the TFRE regrssion with SCAD penalty.

Noneifsecond_stageis notscad.- Returns:

Beta_TFRE_scad (np.ndarray([k,p+1])) – The estimated coefficient matrix of the TFRE SCAD regression. The diminsion is k x (p+1) with the first column to be the intercepts, where k is the length of

eta_listvector.df_TFRE_scad (np.ndarray([k,])) – The number of nonzero coefficients (intercept excluded) for each value in

eta_list.eta_list (np.ndarray([k,])) – The tuning parameter vector used in the TFRE SCAD regressions.

hbic (np.ndarray([k,])) – A numerical vector of HBIC values for the TFRE SCAD model corresponding to each value in

eta_list.eta_min (float) – The eta value which yields the smallest HBIC value in the TFRE SCAD regression.

beta_TFRE_scad_min (np.ndarray([p+1,])) – The estimated coefficient vector which employs

eta_minas the eta value in the TFRE SCAD regression.

- coef(s)[source]¶

Extract coefficients from a fitted

TFREclass.- Parameters:

s (str, optional) – Regression model to use for coefficient extraction. Should be one of

"1st"and"2nd".- Returns:

The coefficient vector from the fitted

TFREclass, with the first element as the intercept.- Return type:

np.ndarray([p+1,])

Notes

If

second_stage = None,scannot be"2nd". Ifsecond_stage = Noneands = "2nd", the function will return the coefficient vector from the TFRE Lasso regression. Ifsecond_stage = "scad"or"mcp", ands = "2nd", the function will return the coefficient vector from the TFRE SCAD or MCP regression with the smallest HBIC.Examples

>>> import numpy as np >>> from TFRE import TFRE >>> n = 100 >>> p = 400 >>> X = np.random.normal(0,1,size=(n,p)) >>> beta = np.append([1.5,-1.25,1,-0.75,0.5],np.zeros(p-5)) >>> y = X.dot(beta) + np.random.normal(0,1,n) >>> >>> obj = TFRE() >>> obj.fit(X,y,eta_list=np.arange(0.09,0.51,0.03)) >>> >>> obj..coef("1st")[:10] array([-0.12943468, 1.21390299, -0.82102807, 0.56632981, -0.20740154, 0. , 0. , 0. , 0. , 0. ]) >>> obj..coef("2nd")[:10] array([-0.13552865, 1.63426996, -1.13200778, 1.1699545 , -0.47397631, 0.17350995, 0. , 0. , 0. , 0. ])

- est_lambda(X=None, alpha0=0.1, const_lambda=1.01, times=500)[source]¶

Estimate the tuning parameter for a TFRE Lasso regression given the covariate matrix X.

- Parameters:

X (np.ndarray([n,p])) – Input matrix of the regression.

alpha0 (float, optional, default = 0.1) – The level to estimate the tuning parameter.

const_lambda (float, optional, default = 1.01) – The constant to estimate the tuning parameter, should be greater than 1.

times (int, optional, default = 500) – The size of simulated samples to estimate the tuning parameter.

- Returns:

The estimated tuning parameter of the TFRE Lasso regression given X.

- Return type:

float

Examples

>>> import numpy as np >>> from TFRE import TFRE >>> n = 100 >>> p = 400 >>> X = np.random.normal(0,1,size=(n,p)) >>> obj = TFRE() >>> obj.est_lambda(X) [0.43150559039112646]

- fit(X=None, y=None, alpha0=0.1, const_lambda=1.01, times=500, incomplete=True, const_incomplete=10, thresh=1e-06, maxin=100, maxout=20, second_stage='scad', a=3.7, eta_list=None, const_hbic=6)[source]¶

Fit a TFRE regression model with Lasso, SCAD or MCP regularization.

- Parameters:

X (np.ndarray([n,p])) – Input matrix of the regression.

y (np.ndarray([n,])) – Response vector of the regression.

alpha0 (float, optional, default = 0.1) – The level to estimate the tuning parameter.

const_lambda (float, optional, default = 1.01) – The constant to estimate the tuning parameter, should be greater than 1.

times (int, optional, default = 500) – The size of simulated samples to estimate the tuning parameter.

incomplete (bool, optional, defaule =

True) – IfTrue, the Incomplete U-statistics resampling technique would be applied in computation. IfFalse, the complete U-statistics would be used in computation.const_incomplete (int, optional, default = 10) – The constant for the Incomplete U-statistics technique. If ` incomplete = TRUE`,

const_incompletex n samples will be randomly selected in the coefficient estimation.thresh (float, optional, default = 1e-6) – Convergence threshold for QICD algorithm.

maxin (int, optional, default = 100) – Maximum number of inner coordiante descent iterations in QICD algorithm.

maxout (int, optional, default = 20) – Maximum number of outter Majoriaztion Minimization step (MM) iterations in QICD algorithm.

second_stage (str, optional, default =

"scad") – Penalty function for the second stage model. One of"scad","mcp"and"none".a (float, optional, default = 3.7, suggested by Fan and Li (2001)) – an unknown parameter in SCAD and MCP penalty functions.

eta_list (float, optional, default = 3.7, suggested by Fan and Li (2001)) – A numerical vector for the tuning parameters to be used in the TFRE S CAD or MCP regression. Cannot be

Noneifsecond_stage = "scad"or"mcp".const_hbic (int, optional, default = 6) – The constant to be used in calculating HBIC in the TFRE SCAD regression.

- Returns:

self – a fitted

TFREclass with attributes “model”, “TFRE_Lasso”, “TFRE_scad” (ifsecond_stage = "scad"), and “TFRE_mcp”(ifsecond_stage = "mcp").- Return type:

object

- class model(X, y, incomplete, second_stage)[source]¶

a class used to record the regression details.

- Returns:

X (np.ndarray([n,p])) – Input matrix of the regression.

y (np.ndarray([n,])) – Response vector of the regression.

incomplete (bool) – If

True, the Incomplete U-statistics resampling technique would be applied in computation. IfFalse, the complete U-statistics would be used in computation.second_stage (str) – Penalty function for the second stage model. One of

"scad","mcp"and"none".

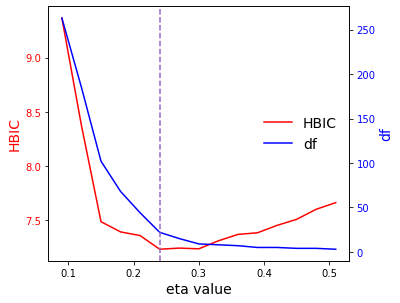

- plot()[source]¶

Plot the second stage model curve for a fitted

TFREclass.- Returns:

This function plots the HBIC curve and the model size curve as a function of the

etavalues used, from a fitted TFRE SCAD or MCP model.- Return type:

Figure

Notes

In the output plot, the red line represents the HBIC curve as a function of

etavalues, the blue line represents the number of nonzero coefficients as a function ofetavalues, and the purple vertical dashed line denotes the model selected with the smallest HBIC.This function cannot plot the object if

second_stage = None.Examples

>>> import numpy as np >>> from TFRE import TFRE >>> n = 100 >>> p = 400 >>> X = np.random.normal(0,1,size=(n,p)) >>> beta = np.append([1.5,-1.25,1,-0.75,0.5],np.zeros(p-5)) >>> y = X.dot(beta) + np.random.normal(0,1,n) >>> >>> obj = TFRE() >>> obj.fit(X,y,eta_list=np.arange(0.09,0.51,0.03)) >>> obj.plot()

- predict(newX, s)[source]¶

Make predictions from a fitted

TFREclass for new X values.- Parameters:

newX (np.ndarray([\(n_0\),p])) – Matrix of new values for X at which predictions are to be made.

s (str, optional) – Regression model to use for prediction. Should be one of

"1st"and"2nd".

- Returns:

The vector of predictions for the new X values given the fitted

TFREclass.- Return type:

np.ndarray([\(n_0\),])

Notes

If

second_stage = None,scannot be"2nd". Ifsecond_stage = Noneands = "2nd", the function will return the predictions based on the TFRE Lasso regression. Ifsecond_stage = "scad"or"mcp", ands = "2nd", the function will return the predictions based on the T FRE SCAD or MCP regression with the smallest HBIC.Examples

>>> import numpy as np >>> from TFRE import TFRE >>> n = 100 >>> p = 400 >>> X = np.random.normal(0,1,size=(n,p)) >>> beta = np.append([1.5,-1.25,1,-0.75,0.5],np.zeros(p-5)) >>> y = X.dot(beta) + np.random.normal(0,1,n) >>> >>> obj = TFRE() >>> obj.fit(X,y,eta_list=np.arange(0.09,0.51,0.03)) >>> >>> newX = np.random.normal(0,1,size=(10,p)) >>> obj.predict(newX,"2nd") array([ 2.61684897, 2.66548778, -0.13456993, -0.67466848, 3.92941648, 1.21428428, -1.66033086, -2.13238483, 0.95340816, -2.32122001])